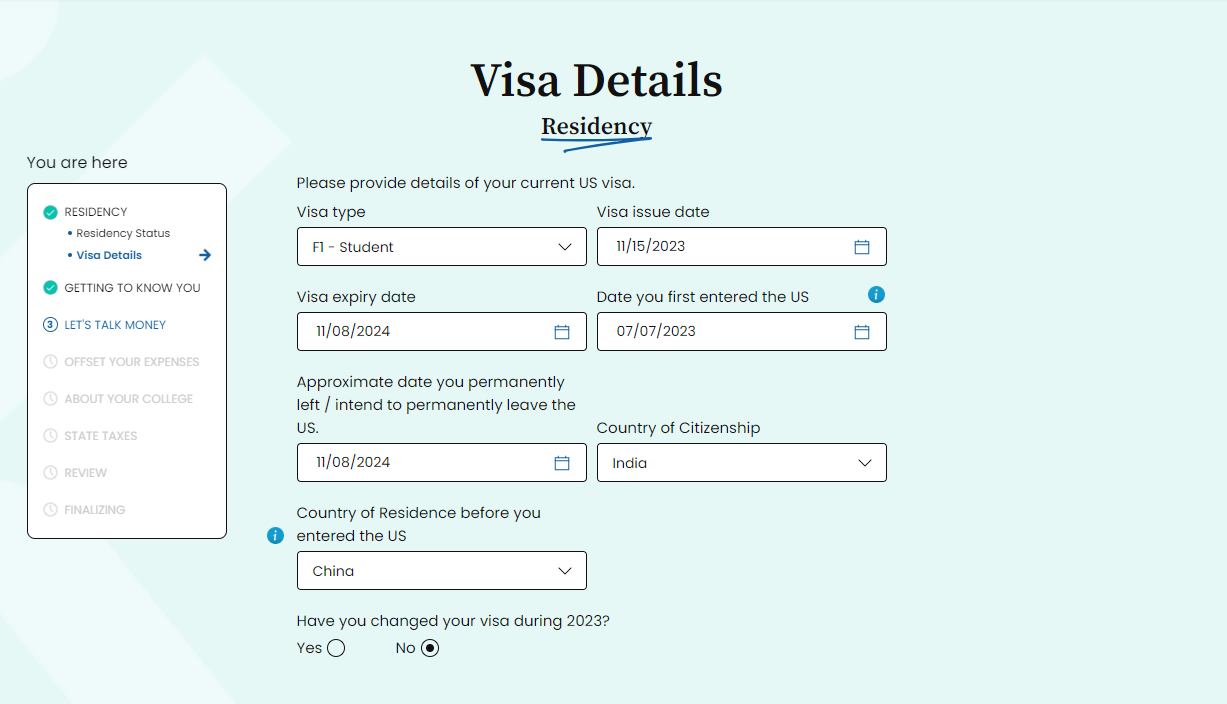

To qualify for any benefits under the US-China Tax Treaty, your country of residence prior to entering the US must have been China. You provide that information in Step 1 "Residency", "Visa Details".

Info: Country of Residence before you entered the U.S. refers to the country where you were a tax resident before arriving in the U.S. Please be aware that your country of residence may differ from the country of your citizenship.

1. Tax Treaty Article 20(b) for Scholarship or fellowship grants.

1.1. Your Visa status on Sprintax must be one of the following:

- Research scholar

- Scholar/Short-Term Scholar

- Intern/Trainee

- Student and full-time student or scholar in a US educational institution

- Vocational Student

- Q1 OR Q2 Trainee

- Researcher

|

Therefore, someone with a different Visa type, as shown on the screenshot below, might not be able to avail of any benefits under Tax Treaty Article 20(b).

Important: If you are an international student in the U.S., you can benefit from Article 20(b) only if you are enrolled as a full-time student at a U.S. educational institution.

1.2. You must've received a scholarship reported on form 1042-S with Income Code 16 under Box 1.

Article 20(b) allows you to exclude the entire amount of the scholarship you received from your gross income, so you won't owe any tax on it. However, Article 20(b) will not apply if you have no scholarship reported on a 1042-S form.

1.3. In order to avail the benefits of Article 20(b) your scholarship must be paid by one of the following entities:

- Governmental institution

- Religious institution

- Educational institution

- Scientific or Academic research institution

- Charitable institution

|

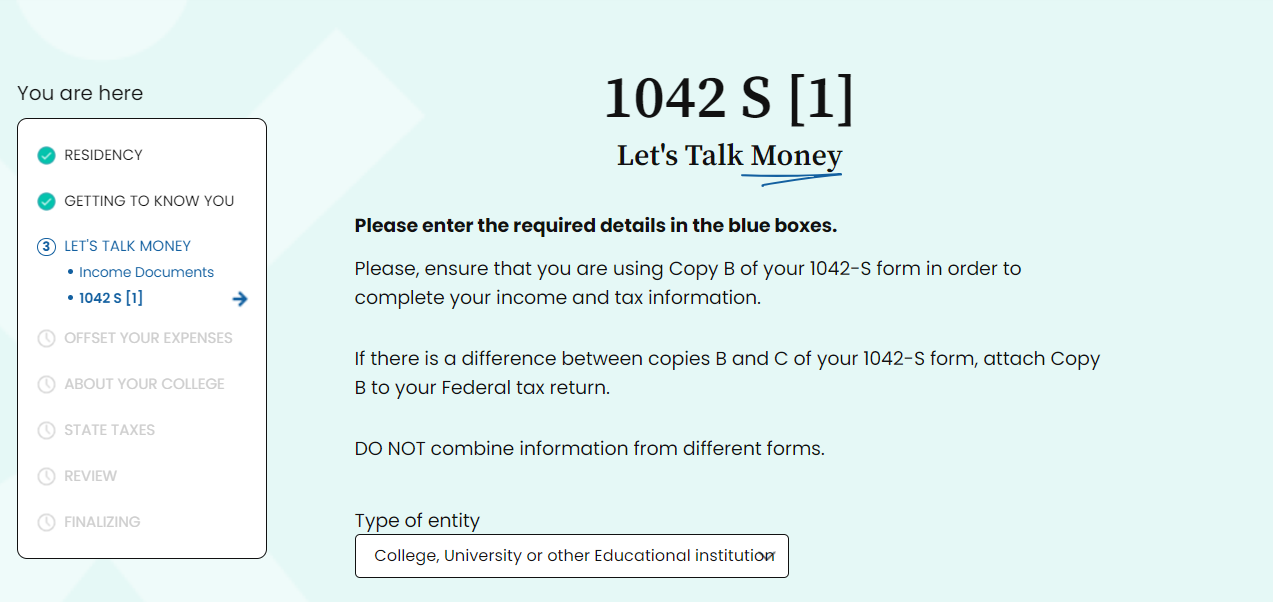

Your can select the type of entity on Step 3, "Let's Talk Money", 1042-S. Any other payers do not qualify for the benefits under Article 20(b).

2. Tax Treaty Article 20(c) for compensation received during study or training.

2.1. Your Visa status on Sprintax must be one of the following:

- Intern/Trainee

- Q1 OR Q2 visa

- Vocational student

- Student

|

Therefore, someone with a different Visa type, as shown on the screenshot below, might not be able to avail of any benefits under Tax Treaty Article 20(c).

Important: Students can avail of the benefits under Article 20(c) as long as their student status is valid in the US.

2.2. You must've received income from compensation during study or training reported on a W-2 form or on a 1042-S form with Income Code 20 under Box 1.

Article 20(c) allows you to exclude the first $5,000 earned from your gross income, so you won't owe any tax on it. However, Article 20(c) does not apply to types of income that are unrelated to compensation received during study or training.

3. Tax Treaty Article 19 for compensation for teaching or research.

3.1. Your Visa status on Sprintax must be one of the following:

- Professor/Lecturer/Teacher

- Research Scholar or a Researcher

- Scholar/Short-Term Scholar

|

Therefore, someone with a different Visa type, as shown on the screenshot below, might not be able to avail of any benefits under Tax Treaty Article 19.

3.2. You must've received income from teaching or research reported on a W-2 form or on a 1042-S form with Income Code 19 under Box 1.

Article 19 allows you to exclude the entire amount of your income earned from teaching or research, so you won't owe any tax on it. However, Article 19 does not apply to types of income that are unrelated to compensation for teaching or research.

3.3. In order to avail the benefits of Article 19 your income from teaching or research must be paid by one of the following entities:

- Educational institution

- Scientific or Academic research institution

|

Your can select the type of entity on Step 3, "Let's Talk Money", 1042-S. Any other payers do not qualify for the benefits under Article 19.

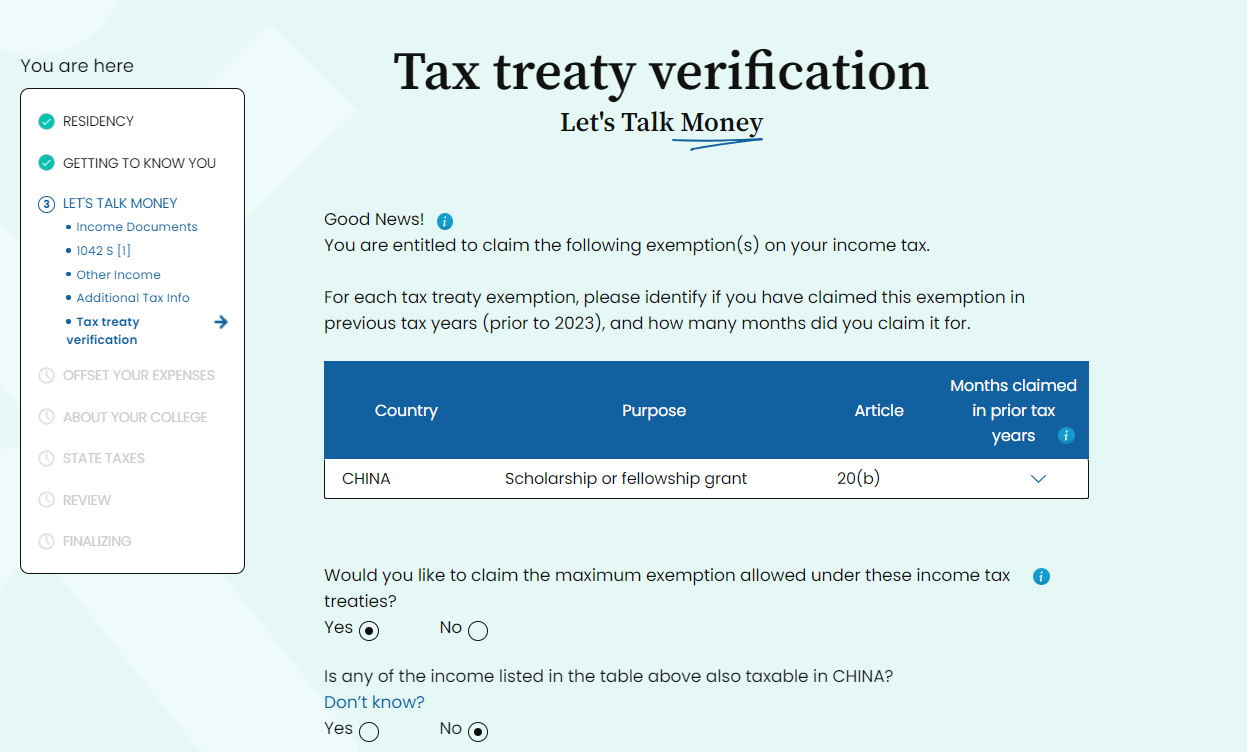

Success: If you meet all the criteria for claiming any Article of the U.S.-China Tax Treaty, Step 3, "Let's Talk Money" will include a Tax Treaty Verification sub step for you. By answering "Yes" to the question about claiming the maximum exemption allowed, you will be electing to use all associated tax benefits of the US-China Tax Treaty, which are allowed based on your personal information, on your 1040-NR Federal tax return.

Info: For months claimed in previous Tax Years, please specify the number of months for which you claimed the Tax Treaty on your prior tax returns. Do not include any months from the current Tax Year for which you are applying.

Info: Regrettably, we are unable to advise whether the income exempted under the tax treaty would be taxable in your home country. This determination relies on the taxation system of your home country. Nonetheless, remember that on your US Federal tax return, this information is solely provided for informational purposes.

Important: If certain tax treaty articles are missing on this step, it indicates that you do not meet the relevant criteria to claim them. If this step is entirely unavailable, it means you do not meet the requirements under any article of the US-China tax treaty convention.